Are you curious about how to build credit? At Greater Nevada Credit Union, we’re committed to helping our members take control of their credit and achieve financial success. Whether you’re just starting or want to improve your current score, we offer different tools and resources to guide you every step of the way.

How to Build Credit

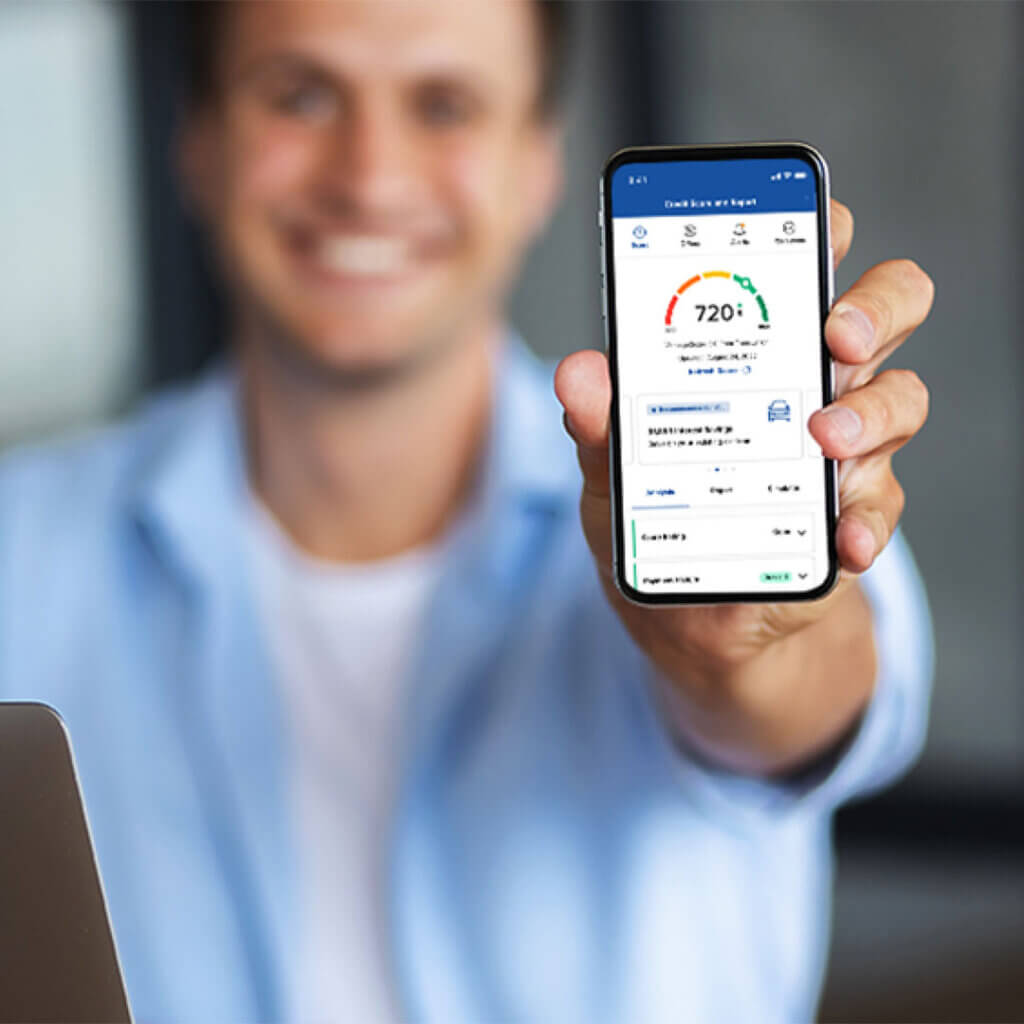

My Credit Health – Free to All Members!

My Credit Health is an all-in-one credit tool fully integrated within Greater Nevada Digital Banking that lets you monitor, manage, and improve your credit.

Over 37,300 members have strengthened their financial future, either by moving up to or keeping their top-tier standing since using it!

Amount is based on active members enrolled in My Credit Health for at least 6 months who are qualified as Credit Savvy as of July 2026. Members must be at least 18 years old to use My Credit Health.

What is a Credit Score?

A credit score is a three-digit number, typically 300 to 850, reflecting your creditworthiness. It’s calculated based on various credit scoring factors, including your payment history, the total amount of debt you owe, the length of your credit history, the types of credit you use, and recent credit inquiries.

Lenders use this score as a quick reference to assess the level of risk involved in lending to you. The higher your credit score, the more likely you’ll get approved for loans, credit cards, mortgages, and other forms of credit, often at more favorable interest rates and terms. On the other hand, a lower score may signal to lenders that you’re a higher risk, which can result in higher interest rates, less-than-ideal terms, or application denial.

Types of Credit

When learning how to build credit, knowing the two main types available to borrowers is essential.

Revolving Credit

Includes credit cards and lines of credit. You can borrow up to a set limit, repay, and borrow again.

Installment credit

Includes loans like auto, mortgage, and student loans. You borrow a fixed amount and repay it over time with regular payments.

How to Build Credit in 7 Ways

One of the most important factors in building and maintaining good credit is paying your bills on time. Late payments can have a negative impact on your credit score. To help you stay on track, consider setting up automatic payments or reminders.

You can use our free Bill Pay feature in Greater Nevada Digital Banking to manage recurring payments easily and ensure you’re always on time. It’s a simple way to keep your finances in order and protect your credit.

Credit utilization ratio is your total credit used divided by the total credit available to you. To maintain a healthy credit score, it’s best to keep your utilization below 30%.

Learn more about managing your credit utilization ratio in our blog post.

Having a variety of credit types—such as credit cards, auto loans, and mortgages—can positively impact your credit score. This shows lenders that you can manage different forms of credit responsibly. A healthy credit mix of both revolving and installment credit accounts can improve your creditworthiness over time.

Being added as an authorized user on someone else’s credit card can help you build credit without being the primary account holder. The card’s payment history and credit utilization will be reported on your credit profile, helping to improve your score. It’s a useful option for those looking to establish or enhance their credit.

The length of your credit history matters. Keeping older accounts open, even if they aren’t used frequently, can positively impact your score by showing a longer credit history.

A secured credit card is one effective way to establish credit and build a good credit score by depositing funds into a secured savings account. The account serves as collateral for the credit line and is used if the borrower cannot repay.

Using a secured credit card responsibly can help improve your credit score because your payments are reported to the credit bureaus. Choose a secured card that fits your spending habits to maximize your benefits, and it’s crucial to make your payments on time to avoid late fees and negative impacts on your credit scoring factors. This approach can also help you qualify for an unsecured credit card in the future.

One of the simplest ways to improve your credit score is by reviewing your credit reports for errors. Even small inaccuracies can negatively impact your credit. You can access free copies of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year at AnnualCreditReport.com. Alternatively, you can request a report directly from each bureau for a small fee.

If you spot any errors on your credit reports, it’s important to dispute them with the appropriate credit reporting agency. The Consumer Financial Protection Bureau (CFPB) provides helpful resources for addressing these errors, ultimately improving the factors that affect your credit score.

Other Resources on How to Build Credit

Live Greater Blog

Greater financial know-how can lead to many opportunities for your family, friends, and (of course) you! Browse through our various financial & lifestyle tips to help you thrive.

Blog

Webinars & Events

GNCU is proud to offer and partner on free financial wellness webinars and in-person events to members and non-members throughout Nevada and beyond.

Webinars & Events

Financial Calculators

Make smarter money decisions fast by exploring our free financial calculators to plan, compare, and stay in control of your finances.

Financial Calculators

Ready to Build Credit With Greater Nevada?

At Greater Nevada Credit Union, we offer reliable tools and expert guidance to help you take control of your credit. Whether you’re looking to improve your credit score or just getting started, we’re here to provide the resources and support you need for a more secure financial future.