Greater Nevada offers loans with competitive rates and flexible terms for almost every budget. Explore our Nevada loans today.

Loans & Credit

Jump-start Your Dreams with Greater Nevada Credit Union

90 Days With No Payments on New and Used Auto Loans*

Looking for a new (or new to you) car, truck, or van? Start here with a low rate and a limited-time offer of no payments for the first three months. Then, hit the road anywhere!

*90-day no pay offer is based on approved credit. Offer is available for auto loans with application submitted by September 30, 2025. Payment Saver Auto Loans are not eligible. If accepted, it will extend your loan by three (3) months, and finance charges will accrue on unpaid principal. Offer is subject to change or cancellation without notice except as required by law.

Why Greater Nevada Credit Union Loans Are Right For You

Competitive Rates

Greater Nevada offers an array of competitive rates and corresponding monthly payments to suit your needs.

Flexible Loans

Most Greater Nevada loans offer different options to help best fit your situation, because customizable loans can help more people Live Greater.

No Hidden Fees

With some of the lowest rates in the state, you can also borrow with the confidence that everything will be clearly explained throughout the process.

It’s Easy to Apply

You can choose to submit your application online, or you can handle it over the phone with an expert loan consultant.

Compare Greater Nevada Credit Union Loan & Credit Options

Let’s talk about your dreams. Planning to finally buy that RV and travel across the country? Or perhaps go all in on that electric vehicle you’ve wanted for years? Whether you’re searching for a credit card, line of credit for your home or a loan to cover an emergency, Greater Nevada has a variety of options — including flexible loan amounts, loan terms and competitive interest rates — to fit your needs.

Auto Loans

Reliable auto loans so you can get behind the wheel in your new (or new to you) car or truck. We even have resources to help you choose your new ride.

Mortgage Loans

Ready to turn home dreams into a home reality? Explore Greater Nevada’s competitive rates and terms for home loans.

Home Equity Lines of Credit (HELOC)

A Home Equity Line of Credit (HELOC) from Greater Nevada leverages the equity in your home and provides you with a line of credit to tap into when you need it.

Personal Loans

Unexpected (or expected) expenses crop up? Life happens, but it doesn’t have to throw you off course. See about Greater Nevada’s personal loans and debt consolidation options.

Personal Loans

Personal Lines of Credit (PLOC)

Thinking you may need access to funds down the road? A Greater Nevada personal line of credit lets you tap into money only as you need it.

Personal Lines of Credit

Credit Cards

With contactless payments and different reward options available, Greater Nevada’s credit cards are designed for the way you live.

Credit Cards

Recreational Vehicle Loans

Boats, RVs, travel trailers, motorcycles, ATV/UTVs: whatever your plans, we’re here to help find the right recreational loan you can afford.

Recreational Vehicle Loans

RV Loans

When it’s time to explore the wonders of America, there’s nothing better than an RV for doing so. Explore a Greater Nevada recreational vehicle (RV) loan with payments that can fit your budget.

RV Loans

Motorcycle Loans

Get your motor runnin’, then cruise the cities, highways and backroads across the nation with a Greater Nevada motorcycle loan.

Motorcycle Loans

Boat Loans

Tahoe, Pyramid and Lake Mead are calling. Dream big and get out on the water with a Greater Nevada recreational boat loan today.

Boat Loans

Vacant Land & Lot Loans

Securing your piece of the Nevada dream with a land loan is the perfect start for your future haven.

Land Loans

Deposit Secured Loans

Leverage your savings deposits or share certificates as collateral for a loan, while still earning dividends.

Deposit Secured Loans

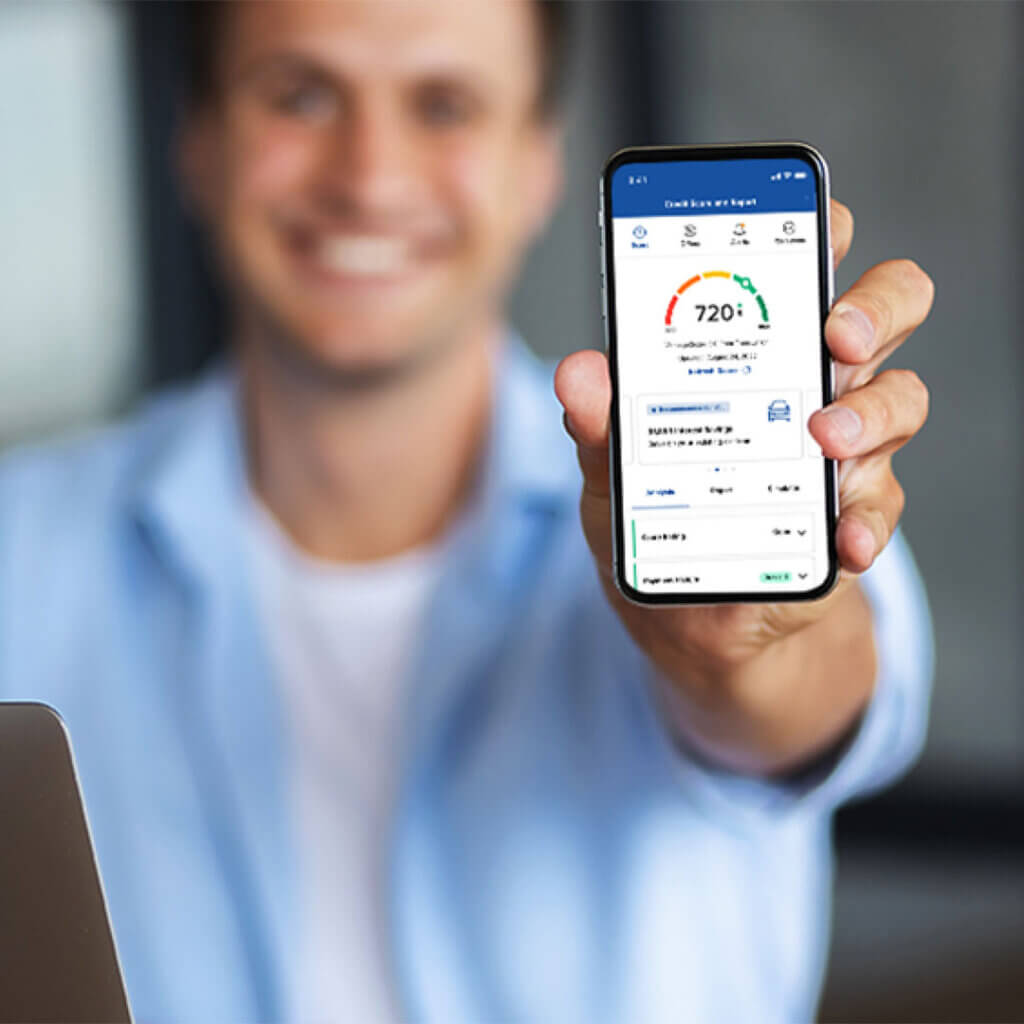

My Credit Health – Free to All Members!

My Credit Health is an all-in-one credit tool fully integrated within Greater Nevada Digital Banking that lets you monitor, manage, and improve your credit.

Over 33,100 members have increased their credit score tier or maintained their top-tier credit score since using it!

Amount is based on active members who have been enrolled in My Credit Health for at least 6 months as of April 2025. Members must be at least 18 years old to use My Credit Health.

A Streamlined Loan Application Process

At Greater Nevada, we believe the loan application process should be a pleasant one. Note that each loan type will have its own terms, funding process and requirements along with pulling your credit report.

1. Determine Loan Needs

The type of loan you’re seeking — be it auto, home or personal — will determine the amount you need to borrow.

2. Compare Loan Types

Explore Greater Nevada’s flexible and affordable loans to fit what you need.

Gather Documents Needed

Required paperwork will vary by loan type, but generally we need to verify your credit history along with your income and residency.

4. Apply for a Loan

Pick the way that work best for you: apply for an online loan through your computer or other device, or over a phone call with a loan consultant will be in touch to work with you on options available.

Debt Consolidation Loan

Don’t float bills by using high-interest credit cards. Explore how you could lower your monthly payments and bring all your bills together into a single payment with a debt consolidation loan from Greater Nevada.

What is the easiest loan to get approved for?

Is it hard to get a loan from a credit union?

Is it better to get a loan through a credit union?

What credit score do you need to get a personal loan at a credit union?

How much can you borrow from a credit union?

Real Members, Real Impact

We are a community of people who are committed to helping each other. Our Live Greater Stories series highlights the passions, lives, and businesses of our members, and the ways in which we helped them meet their goals and fulfill their dreams.

We’re Here to Help

Apply for a Greater Nevada Credit Union Loan

Ready to get started on your loan application? Get started below.